By Richard Galant

When Frances Perkins became the first woman to serve in a president’s Cabinet in 1933, she knew her role wouldn’t be easy.

“I tried to have as much of a mask as possible,” she later said about her first Cabinet meeting. “I wanted to give the impression of being a quiet, orderly woman who didn’t buzz-buzz all the time. … I just proceeded on the theory that this was a gentleman’s conversation on the porch of a golf club perhaps. You didn’t butt in with bright ideas.”

But that didn’t last long: she helped develop plenty of bright ideas as secretary of labor. Not least was Social Security.

“Out of our first century of national life we evolved the ethical principle that it was not right or just that an honest and industrious man should live and die in misery. He was entitled to some degree of sympathy and security,” she argued. Perkins stood behind President Franklin D. Roosevelt when he signed the Social Security Act in 1935, the only woman in the now historic photos of the event.

The program’s maximum monthly benefit was set at $85 — equivalent to about $1,856 in today’s dollars. Life expectancy for Americans then was several years below the minimum retirement age of 65 for collecting benefits.

Today, the maximum monthly benefit is $3,627 for those retiring at the standard age of 67. Babies born now can expect to live 12 years longer.

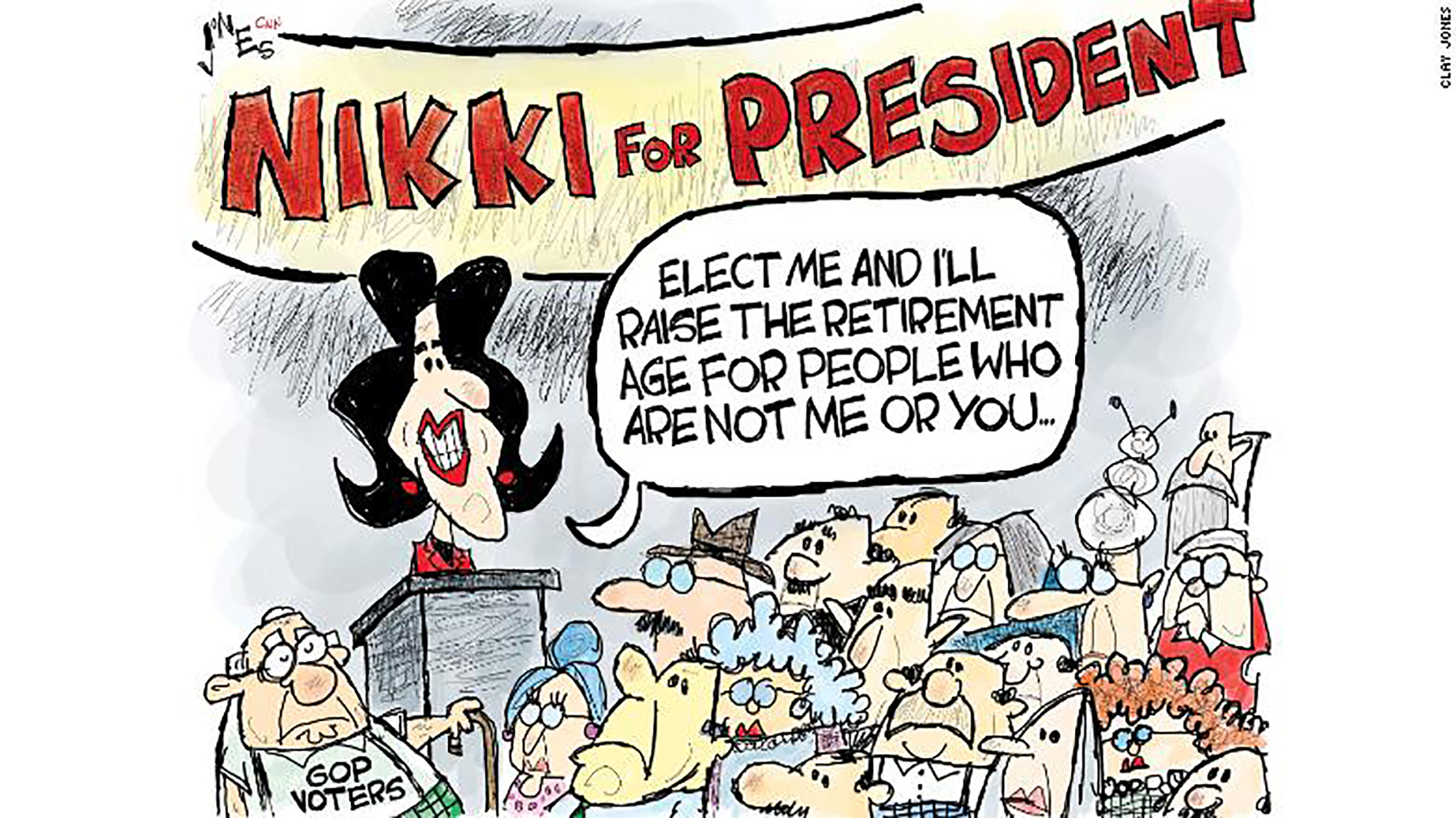

For those who believe that the math no longer works and Social Security is now unsustainable — benefits could be cut by at least 20% within a decade if nothing is done, experts say — Republican presidential candidate Nikki Haley offered a solution last week. She called for raising the retirement age for people now in their 20s and limiting benefits for the wealthy.

In tackling the issue, Haley became the rare candidate willing to touch the “third rail” of American politics, explained Julian Zelizer. “It is not surprising that Republicans like former President Donald Trump have already attacked fellow GOP candidates for wanting to raise the retirement age or cut Medicare, while others in the party are scrambling to distance themselves from a House Republican Caucus that is pushing for draconian cuts to domestic programs.”

“For it is one thing to tell Americans that Washington is broken and another to say they will slash the federal benefits upon which so many of them have come to depend,” he added.

President Joe Biden’s budget, released last week, calls for $3 trillion in deficit reduction over 10 years, but no one expects that Republicans will provide the votes needed to pass the president’s proposal to increase taxes on billionaires, corporations and high-income earners to help make that happen. And Biden didn’t touch Social Security, demonstrating a rare alignment with Trump, who in January said, “Under no circumstances should Republicans vote to cut a single penny from Medicare or Social Security.”

Maya MacGuineas, who heads the Committee for a Responsible Federal Budget, observed that “neither President Biden nor those before him have done much of anything to address or fund the rising costs of our nation’s major health and retirement programs. And in the end, the buck stops at the top.” She argued that even if Biden could slice $3 trillion off the deficit, it would not be “enough to fix the debt dangers we face. Not even close.”

House Republicans are insisting on spending cuts in return for raising the nation’s debt limit. That’s a dangerous error, wrote economists Mary E. Lovely and Katheryn Russ. “Failure to raise the debt limit would weaken our national security because it is precisely the world’s trust and confidence that the United States government will pay its debts in full and on time that helps keep the dollar as the world’s dominant currency,” they argued.

“The responsible way to control growth in the national debt is by raising taxes and cutting spending in a process of budget negotiations based on good faith.”

The debt ceiling standoff is causing concern on Wall Street. So is last week’s sudden failure of Silicon Valley Bank. “Despite the panic over SVB’s collapse, this situation isn’t likely to morph into a broader banking crisis,” wrote economist Darrell Duffie. “Since the collapse of Lehman Brothers in 2008, the largest US banks have been forced by regulators to be much more resilient. They also rely far more heavily than SVB on retail depositors, who tend to have a greater share of their deposits covered by FDIC insurance and are less prone to run at the first sign of trouble.”

“Of more immediate concern is the potentially systemic impact this will have on the tech sector, which has already seen mass layoffs and investments shrivel up in recent months. Close to half of all listed US venture-backed tech and health care firms were SVB customers and many of these companies were racing to line up funds to make payroll in the aftermath of the collapse.”